VP Bank shares

Economic environment in 2016

2016 was a politically eventful year. In June, British voters opted to exit the European Union and in November Donald Trump won the U.S. presidential election. Financial markets appeared to take both electoral outcomes in stride, thanks in part to an improving global economic outlook in the second half of 2016. Growing confidence in the economies of commodity-exporting emerging countries as a result of rising oil prices as well as stable growth rates in China were the most notable factors underpinning the favourable news flow.

In the United States, growth was initially weak in the first half but the world’s largest economy regained momentum in the second. The US labour market nevertheless performed well throughout the year, as job growth continued its upward trend in 2016. The unemployment rate fell from 5 per cent at the start of the year to 4.7 per cent at the end. These gains in employment ultimately led to rising wages. Given rising oil prices that pushed inflation higher and the lack of negative consequences from Donald Trump’s victory, as had been widely feared, the US central bank responded by raising rates for the second time in the current monetary tightening cycle.

The euro zone economy proved to be surprisingly robust. Despite fears of economic collapse in the event of a pro- Brexit vote during the period leading up to the referendum, the real economy responded to the event relatively calmly. In the United Kingdom, economic sentiment even brightened considerably in autumn, as British companies welcomed the significant slide in the pound and improved competitiveness in the wake of the Brexit vote. No further economic damage was felt on the European Continent either, such that the impact of the UK referendum has been only theoretical so far. The consequences will only become apparent once the contractual parameters of the future relationship between the United Kingdom and European Union are known and the actual exit occurs.

Even though inflation rates in the euro zone inched slightly higher during the autumn months, the European Central Bank (ECB) opted to continue its expansive monetary policy. Adjusted for the energy price component, inflation remained at a standstill. ECB President Mario Draghi is therefore expected to continue monthly securities purchases – albeit at a slower pace – through end-2017. The divergent monetary policies on either side of the Atlantic put further pressure on the euro against the US dollar. In December 2016, the EUR/USD exchange rate was only slightly above parity.

The state of the Swiss economy can best be described as “light at the end of the tunnel”. After a challenging year in 2015 following the sharp rise in the Swiss franc, the economy rebounded in 2016. The country’s export economy even managed to recover as companies squeezed profit margins. The deflationary phase also bottomed out. In December, inflation was flat, marking more than two years without any negative signs. With upward pressure still evident on the Swiss franc, the SNB took advantage of the lack of deflationary effects as well as the substantially improved company sentiment to tolerate a slight appreciation in the Swiss currency. The overall monetary policy orientation nevertheless remained unchanged throughout 2016. While the SNB continued to intervene in currency markets, it did not need to adjust interest rates.

Equity markets in 2016

From a geopolitical and macro-economic perspective, 2016 was a very eventful year. Early on, many investors focused on economic issues such as the threat of weaker economic growth in China and the accompanying deflationary effects. With the Brexit vote, this focus nevertheless shifted increasingly toward political concerns and reached its zenith with the election of Donald Trump as the 45th US president. As unexpected as these developments were, the oft-predicted panic selling in equity and bond markets largely failed to materialise despite these huge geopolitical events. Neither Trump and Brexit on the one hand nor continued high valuations with falling earnings and a rising interest rate environment on the other led to any noteworthy or persistent destabilisation.

The MSCI World global equity market index rose by around 8.2% during the past calendar year. This favourable equity price trend was largely driven by emerging country shares, which rose by approximately 11.6 per cent. The most spectacular gains were recorded by Latin American emerging countries, as the relatively robust recovery in crude oil prices led to a veritable surge in equity prices (31.5 per cent). The situation in Europe was less satisfactory. The Euro Stoxx 50 Index, which includes the euro zone’s 50 largest companies, posted only a meagre 4.7 per cent gain while the Swiss Market Index even ended the year on a down note.

For the most part, the rising share prices were not justified by higher earnings and therefore in effect reflect higher valuation.

VP Bank shares

In 2016, VP Bank’s listed bearer shares with a nominal value of CHF 10.00 were converted to registered shares A with the same nominal value. The existing, unlisted registered shares with a nominal value of CHF 1.00 remained as registered shares B and will continue to be unlisted in the future. The first trading day for the registered shares A was 6 May 2016.

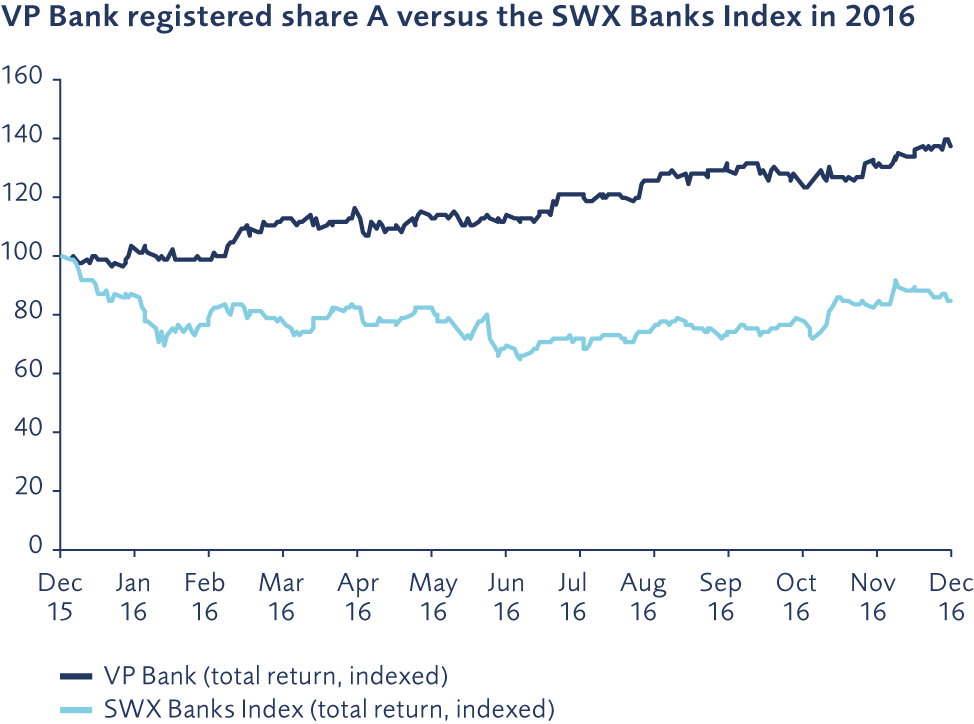

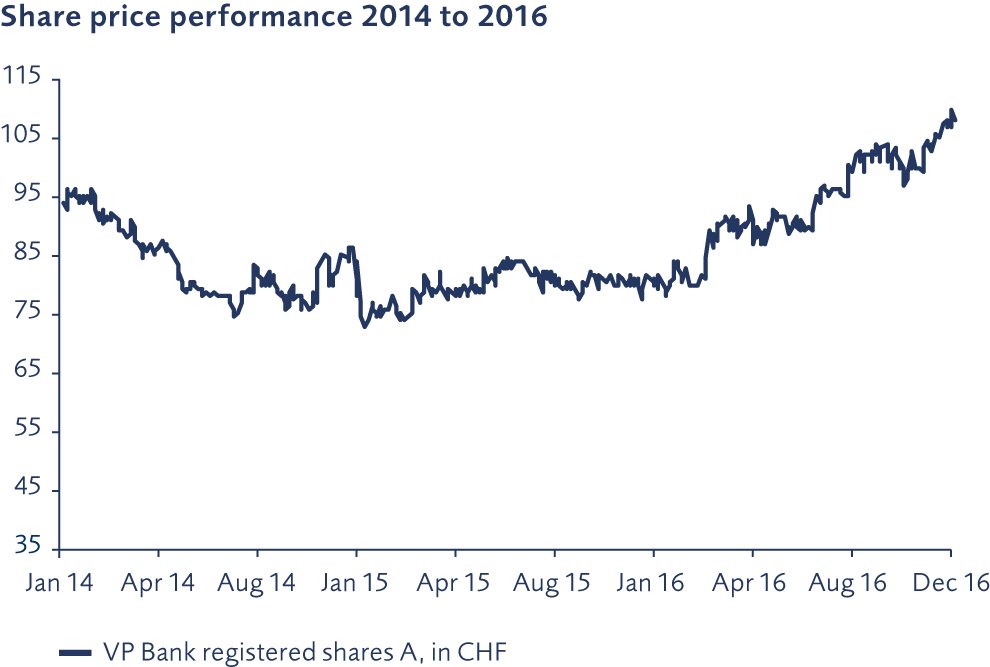

Since end-2012, VP Bank’s shares have recorded significant gains of 66.2 per cent without reinvested dividends and 92.7 per cent with reinvested dividends. These strong returns outperformed both the Swiss Banking Index and the broader Swiss Market Index (SMI) by wide margins. The strongest share price gains occurred in 2013 as well as in 2016. In the period under review, the shares hit their low of CHF 65.00 in January 2013 and reached a high of CHF 111.90 at end- December 2016. Average volatility throughout this period was slightly greater than that of the overall market, but well below that of most competitors.

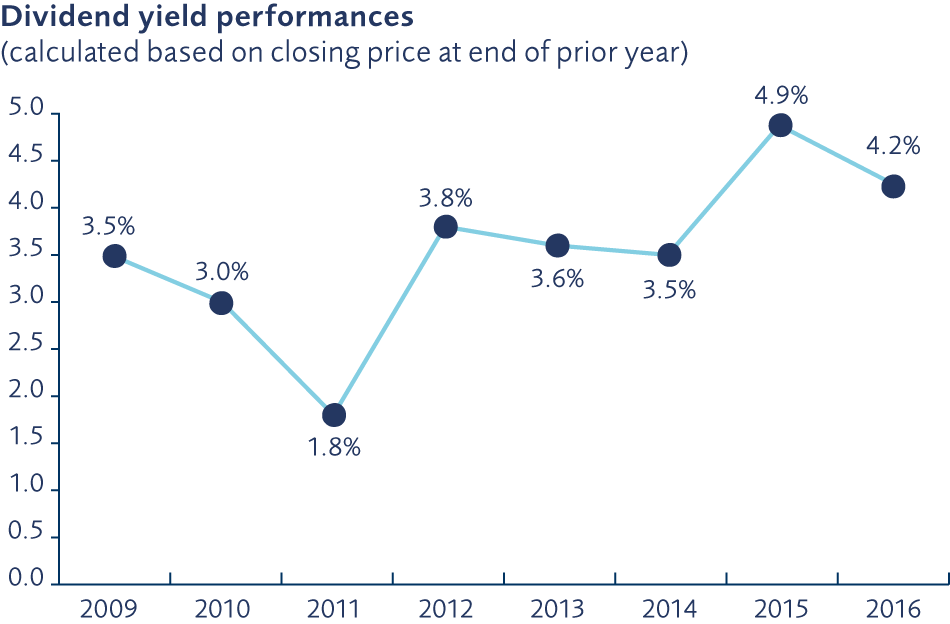

In 2016, VP Bank shares were also among the clear winners. With a 37.1 per cent gain (including dividend), they outperformed both the broader Swiss equity market as well as the Swiss banking sector by 40 per cent and 52 per cent, respectively. The share price performance in 2016 was particularly noteworthy due to its relatively steady upward trend. The low occurred in January (CHF 78.05) and the high in December (CHF 111.90). The average price for the registered shares A was CHF 93.20. In May 2016, VP Bank paid out a dividend of CHF 4.00 per share, which corresponds to a 4.2 per cent dividend yield.

Investor Relations

The goal of VP Bank’s investor relations efforts is to foster an open, ongoing dialogue with shareholders and other capital market participants by providing them with a true and fair view of VP Bank Group, whilst also informing the interested public promptly about the company’s latest developments.

The tasks involved in this investor relations work include conducting discussions with analysts and investors, disclosing ad hoc information regarding business issues of relevance under securities law, producing the company’s annual and interim reports and publishing the related financial results, as well as organising the annual general meeting of shareholders.

For the 54th Annual General Meeting at 28 April 2017, the entire notice and invitation process was overhauled and optimised with the help of a renowned specialist. Shareholders now receive a convenient online announcement and also have the option of early online voting through electronic voting or voting at the meeting through televoting. As part of VP Bank’s digitalisation strategy, these changes led to enhanced convenience, secure anonymity and quicker voting results.

As part of its investor relations activities in 2016, VP Bank held numerous analyst meetings and media conferences in order to further strengthen its communications with investors and financial intermediaries. The 3rd VP Bank Investor Day is scheduled for May 2017 in Luxembourg.

VP Bank’s Investor Relations department is responsible for ensuring the Group’s “Corporate Language”, i.e. a common language used both inside and outside the company in order to speak to all target audiences in one voice. Through the corresponding interfaces, VP Bank ensures that consistent company information is disseminated across the various publications platforms.

VP Bank’s regular presentations on current events lay the foundation for communications with institutional and private investors. The www.vpbank.com website and online annual report available at vpbank.wsc.ch provide all the latest information on the company.

Since 2015, VP Bank’s interim report is also available in an online version.

The continued improvements to VP Bank Group’s annual report, in line with international trends and regulatory requirements, was also emphasized in 2016. The theme of that year’s report was “60 Years of VP Bank.”

The VP Bank Group’s 2015 annual report won a total of five international awards last year, demonstrating the high quality of VP Bank’s information policy as well as its creative design excellence. The bank’s annual report won gold at the ARC Awards for the compelling illustrations surrounding the theme of the company’s 60-year anniversary. The prestigious ARC Awards have been held in the United States for the past 30 years. The annual report also won gold in the US “Stevie Awards” for “Best Annual Report – Print”. Other awards included the “Galaxy Award”, “Vision Award” and “League of American Communications Professionals” (LACP) award.

Meanwhile, VP Bank’s 2015 online annual report received four international awards. For the 2015 Swiss Annual Report Ratings, a jury of communications and finance professionals also placed the VP Bank Group’s annual report in the top 15 in Switzerland and Liechtenstein.

In July 2017, the Standard & Poor’s rating agency confirmed VP Bank’s “A–” rating and raised its outlook from “Negative” to “Stable”. The confirmed rating and improved outlook reflected VP Bank’s operating improvements and prudent risk management as well as the bank’s very strong capital position and its successful integration of Centrum Bank. The favourable Standard & Poor’s assessment cites VP Bank’s ability to generate profitable growth without compromising its capital adequacy. As of 2 March 2017, Standard & Poor’s improved the outlook from “Stable” to “Positive”.

VP Bank therefore holds a rating of “A–/Positive/A–2”. This outstanding rating and the positive outlook confirm the VP Bank Group’s sound and successful business model. VP Bank is one of the few private banks in Liechtenstein and Switzerland to be rated by an international rating agency. The current Standard & Poor’s rating report can be downloaded as a pdf file from the VP Bank website under “Investors & Media”.

Analysts from Mirabaud Securities LLP, Research Partners AG and Zürcher Kantonalbank provide analyses on VP Bank on a regular base.

Agenda |

|

Publication of 2016 annual financial results | Tuesday, 7 March 2017 |

54th ordinary annual general meeting | Friday, 28 April 2017 |

Dividend payment | Friday, 5 May 2017 |

Publication of first-half 2017 financial results | Tuesday, 22 August 2017 |

|

|

|

|

VP Bank share details | |

Registered shares A, listed on SIX Swiss Exchange | |

Number of listed shares | 6'015'000 |

Free float | 44.42 % |

SIX symbol | VPBN |

Bloomberg ticker | VPBN |

Reuters ticker | VPBN.S |

Securities number | 31 548 726 |

ISIN | LI0315487269 |

|

|

|

|

Share-related statistics 2016 | |

High (29.12.2016) | 111.90 |

Low (22.01.2016) | 78.05 |

Year-end close (final settlement value, 30.12.2016) | 108.00 |

Average price | 93.20 |

Market capitalisation in CHF million1 | 714 |

Consolidated net income per registered shares A | 9.61 |

Price Earnings Ratio pro registered shares A | 11.24 |

Dividend per A registered share (proposed) | 4.50 |

Dividend yield (net) in % | 4.2 |

Standard & Poor’s rating2 | A (A–/Stable/A–2) |

- Including registered shares B

- As of 2 March 2017

Further information on the capital structure and anchor shareholders of VP Bank can be found in the “Corporate governance” section.

Contact

Tanja Muster · Head of Group Communications & Marketing

T +423 235 66 55 · F +423 235 65 00