Consolidated annual report of VP Bank Group

Consolidated results

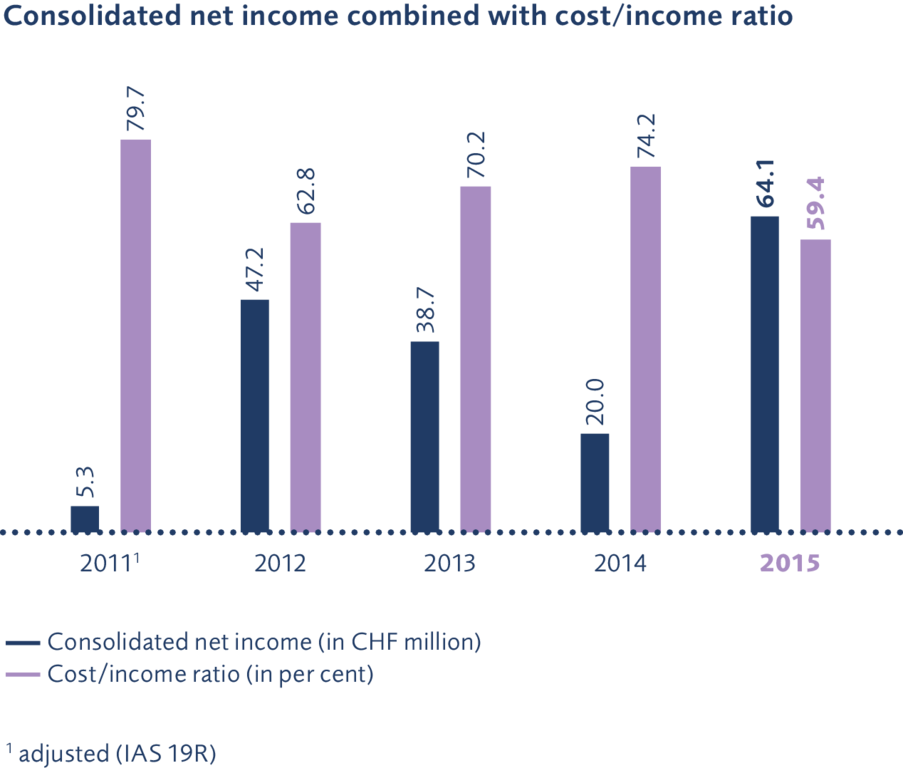

The consolidated financial statements for 2015 of VP Bank Group, prepared in accordance with International Financial Reporting Standards (IFRS), disclose Group net income of CHF 64.1 million. In the prior year, a Group net income of CHF 20.0 million was realised.

The annual results reflect the impact of the merger of VP Bank with Centrum Bank and the associated increase in revenues and expenses. The result is also impacted to a significant degree by the abandonment of the minimum exchange-rate policy of the Swiss franc to the euro as well as the shift in the three monthly Libor target range by the Swiss National Bank (SNB) on 15 January 2015.

Even if the appreciation of the Swiss franc has weakened during the course of the year, it caused a decline in the value of client-related positions denominated in foreign currencies once translated into Swiss francs, the currency in which the balance sheet is expressed. Client assets form the basis for the major share of the revenues of VP Bank Group.

Following the successful consummation of the acquisition in 2014 of the private-banking activities of HSBC Trinkaus & Burkhardt (International) SA and the investment-fund business of HSBC Trinkaus Investment Managers SA in Luxembourg relating to private banking, VP Bank Group continued to pursue its growth strategy with the merger with Centrum Bank in 2015. The merger with Centrum Bank could be successfully completed with the transfer of client data to VP Bank’s IT platform by the beginning of 2016.

Having regard to the annual results and the balanced long-term dividend policy, the Board of Directors will propose a dividend of CHF 4.00 per bearer share and CHF 0.40 per registered share to the annual general meeting to be held on 29 April 2016.

Client assets under management

As of the end of 2015, client assets under management of VP Bank Group totalled CHF 34.8 billion. Compared with the prior year’s comparative of CHF 30.9 billion, this represents an increase of 12.4 per cent.

In 2015, VP Bank Group recorded a net inflow of new client assets of CHF 6.0 billion (prior year: net outflow of CHF 0.9 billion). Of this amount, CHF 6.3 billion relates to the merger with Centrum Bank (CHF 6.7 billion upon acquisition less CHF 0.4 billion of outflows anticipated in the wake of the merger). Net outflows of CHF 0.3 billion were recorded in the operating business. These outflows should be viewed against the backdrop of the regulatory environment and taxation-related issues. On the other hand, welcome inflows of new client assets could be achieved thanks to intensive market-development activities, particularly in Asian markets.

The performance-related decrease in client assets in 2015 amounted to CHF 2.2 billion (prior year: increase of CHF 1.4 billion) resulting from the devaluation of foreign-currency-denominated client assets under management provoked by the discontinuation of the minimum euro exchange-rate policy to the Swiss franc.

Custody assets grew by 7.6 per cent to CHF 8.2 billion (prior year: CHF 7.6 billion).

As of 31 December 2015, client assets including custody assets totalled CHF 43.0 billion (prior year: CHF 38.6 billion).

Income statement

Total operating income

Year-on-year, total operating income grew by 37.7 per cent from CHF 222.7 million to CHF 306.6 million. This increase of CHF 83.9 million is primarily related to the merger of VP Bank with Centrum Bank. Ignoring the effects of the "purchase price allocation", total operating income amounted to CHF 256.6 million.

Interest income rose by 28.9 per cent from CHF 65.6 million to CHF 84.5 million. Net interest income from client-related activities grew as a result of changes in current market conditions. Interest income from financial instruments valued at amortised cost rose by CHF 2.5 million, principally as a result of a higher level of balance-sheet positions. Interest income includes also changes in the value of interest-rate hedging transactions. As a result of the introduction in 2015 of hedge accounting, revaluation losses of CHF 2.8 million could be offset and reduced to CHF 4.2 million (prior year: revaluation losses of CHF 16.0 million).

Income from commissions and services in 2015 again rose by 6.7 per cent to CHF 126.4 million (prior year: CHF 118.4 million). The abandonment of the minimum exchange-rate policy against the euro left its mark on net commission income. As a result of the merger with Centrum Bank, welcome sustainable increases could be achieved in portfolio-based revenues, such as asset management and investment business as well as securities account fees (increase of CHF 12.1 million). Year-on-year, the level of client activities in the securities business declined thus resulting in lower brokerage income. The decline in investment-fund management fees by CHF 4.3 million to CHF 58.5 million, or 6.9 per cent, is linked to foreign-currency-related declines in volumes which spurred also a decline in commission and service-related expense of CHF 1.7 million to CHF 53.9 million.

Income from trading activities in 2015 could be increased from CHF 25.4 million to CHF 46.1 million, or by 81.6 per cent. This increase is to be ascribed to higher volumes of foreign-exchange transactions in the wake of the abandonment of the minimum euro exchange-rate mechanism. A loss of CHF 0.7 million resulted from financial investments (prior year: gain of CHF 12.5 million). Interest and dividend income could be increased by 43.7 per cent to CHF 9.7 million (prior year: CHF 6.7 million) as a result of higher investment volumes. This increase in revenues, however, was unable to offset the revaluation losses resulting from movements in foreign-exchange rates and price reductions.

The gain on the acquisition of Centrum Bank (“bargain purchase”) aggregating CHF 50.0 million resulting from the “purchase price allocation” was recorded in other income.

Operating expenses

Year-on-year, operating expenses increased by CHF 16.8 million from CHF 165.3 million to CHF 182.1 million (increase of 10.2 per cent). This increase is in keeping with the strategic orientation of VP Bank Group and the merger with Centrum Bank.

The growth in personnel expense is a result of the higher headcount in the wake of the merger with Centrum Bank. At the end of 2015, VP Bank Group had 734 employees, expressed as full-time equivalents (prior year: 695). As a result of the change in the conversion factor for the pension fund, personnel expense was credited with a non-recurring amount of CHF 8.5 million. Year-on-year, personnel expense rose by CHF 3.4 million, or 2.9 per cent, to CHF 121.9 million.

General and administrative expenses increased by 28.8 per cent from CHF 46.8 million to CHF 60.2 million in 2015. This increase is a result of the merger with Centrum Bank and the related running of parallel operations for a limited period. Synergies were successively exploited with the integration into the existing infrastructure and process landscape and future associated costs reduced. The merger with Centrum Bank could be successfully completed with the transfer of client data to VP Bank’s IT platform by the beginning of 2016.

Depreciation and amortisation, valuation allowances, provision and losses

Depreciation and amortisation amounted to CHF 38.3 million or some CHF 8.9 million or 30.3 per cent more than the prior year. This increase is primarily due to the amortisation of intangible assets arising on the merger with Centrum Bank.

The charges for valuation allowances, provisions and losses aggregated CHF 26.0 million (prior year: CHF 7.4 million). During the financial year, valuation allowances, provisions and losses for credit risks amounted to CHF 23.2 million (prior year: CHF 12.1 million). The increase of CHF 11.1 mil- lion relates to individual valuation allowances on client credits. At the same time, releases of no longer required valuation allowances and provisions in 2015 increased by 4.8 million from CHF 8.1 million to CHF 12.9 million.

The annual results of 2015 were charged with an amount of CHF 15.3 million for restructuring provisions in connection with Centrum Bank and the operational integration of activities conducted in Luxembourg.

Taxes on income

During 2015, effective taxes on income in an amount of CHF 1.4 million were paid. A minus charge of CHF 3.9 million resulted from the decline in deferred taxation as well as tax-exempt income as a result of the merger with Centrum Bank.

Group net income

Group net income in 2015 amounts to CHF 64.1 million (prior year: CHF 20.0 million). The Group net income per bearer share increased from CHF 3.45 to CHF 10.17 in the 2015 reporting period.

Total comprehensive income

Total comprehensive income encompasses all revenues and expenses recorded in the income statement and under equity. Principally actuarial adjustments relating to pension funds are recorded directly in equity. VP Bank Group achieved a total comprehensive income of CHF 51.9 million as opposed to CHF 0.5 million in the prior year.

Balance sheet

Year on year, total assets grew by CHF 1.2 billion to CHF 12.4 billion. This increase of 10.3 per cent mainly relates to the balance-sheet assets acquired from Centrum Bank. Client liabilities rose similarly to CHF 10.8 billion. On the assets’ side, cash and cash equivalents again increased markedly to CHF 3.0 billion (31.12.2014: CHF 1.9 billion), which reflects a very comfortable liquidity basis of VP Bank. The increase in cash and cash equivalents occurred at the expense of amounts due from banks which declined by CHF 1.2 billion to CHF 2.1 billion. At the same time, financial instruments measured at amortised cost rose by CHF 0.6 billion from CHF 1.1 billion in the prior year to CHF 1.7 billion (plus 55.1 per cent).

Client loans in the caption "due from customers" increased by CHF 0.7 billion to CHF 5.0 billion. This increase is primarily due to the client receivables acquired from Centrum Bank. VP Bank continues unchanged its conservative credit-granting policies focusing on qualitative growth in customer loans as well as a high level of discipline in credit-granting activities. Three fifths of the increase related to mortgage loans and two fifths to credits secured by other types of collateral. Mortgage loans recorded an increase of 14.0 per cent to CHF 3.4 billion.

Consolidated shareholders‘ equity of VP Bank Ltd at the end of 2015 totalled CHF 918.1 million (end of 2014: CHF 868.5 million). This equates to an increase of CHF 49.7 million. Marxer Stiftung für Bank- und Unternehmenswerte participated in the share-capital increase approved at the extraordinary general meeting of 10 April 2015, thus becoming a further anchor shareholder of VP Bank. On the occasion of the annual general meeting of shareholders held on 24 April 2015, the shareholders authorised the Board of Directors to acquire a maximum of 10 per cent of the share capital. VP Bank made use of this authorisation and as of 31 December 2015, holds treasury shares amounting to 9.2 per cent of the share capital.

The tier 1 ratio computed using the new Basel III rules as at 31 December 2015 amounted to 24.4 per cent (31 December 2014, computed using the Basel II rules: 20.5 per cent).

Outlook

2016 has commenced turbulently on financial markets and we assume that 2016 will continue to be a challenging year. This will impact business performance and the results of VP Bank Group. VP Bank is optimally equipped to meet the challenges of the future and will continue to pursue its sustainable growth strategy. The high level of equity resources and stable shareholder base form a healthy basis for VP Bank Group in order to be able to assume an active role in future in the process of consolidation of banks.