VP Bank shares

Economic environment

Yet again, economists set the bar too high in terms of their expectations for 2014. During the course of the year, even major institutions such as the IMF found it necessary to notch down their global growth estimates. In the US, the cold winter caused first-quarter GDP to skid, whereas the prognoses for the US economy had already been revised sharply downwards at the outset of the year. Nonetheless, the very robust trend that set in as the year progressed ultimately resulted in an estimated GDP growth rate of 2.3 per cent for the entire year.

In the Eurozone, the debt-plagued member states managed to continue on their path towards recovery, but the German economy surprisingly hit a few bumps in the road. The sanctions against Russia had an unexpectedly strong impact on the largest domestic economy in the common currency realm. The aggregate GDP growth rate for the entire Eurozone amounted to a mere 0.8 per cent.

Despite the adverse conditions in the neighbouring currency zone, the Swiss economy proved to be extremely resilient. Growth in private consumption and capital spending failed to maintain the pace set in the previous year, but exports were astonishingly robust. In the end, Switzerland’s GDP rose by 1.8 per cent for the year.

On the whole, global trade was once again lethargic, with the export-reliant emerging nations suffering the most. In addition, structural weaknesses burdened GDP growth mainly in the Latin American countries, while the Russian economy took a hard hit from the sanctions imposed by the EU and US. The ruble suffered an unprecedented decline in value. Growth rates in China continued to decelerate: in 2014, the world’s second-largest economy grew by “only” 7.4 per cent.

Inflation rates in the industrialised nations eased considerably in response to the massive decline in oil prices, especially in the second half of the year. This in turn enabled the major central banks to maintain their ultra-expansive monetary policies. But that is not to say that the monetary policy positioning on both sides of the Atlantic failed to change: while the US central bank ended its monthly securities purchases in October 2014 thanks to the solid (domestic) economic underpinnings, the ECB announced a large-scale government bond purchase programme in January 2015. Prior to this announcement, the euro had already lost a huge amount of ground against the US dollar. And just a few days before the ECB’s decision, the SNB disclosed that it intended to abandon the CHF/EUR “floor” of 1.20. That, in turn, triggered violent fluctuations in the foreign exchange, fixed income and equity markets. The Swiss central bankers had already introduced negative interest on the large deposits it holds on behalf of commercial banks in December 2014; it then increased that charge further in January 2015. A normalisation of monetary policy throughout the European continent thus moved further away.

Equity markets

For most equity investors, 2014 was a very successful year. The global stock market, as measured by the MSCI World Index, rose by 5.6 per cent for the year (including dividends). Whilst the trend in the US was driven primarily by higher corporate earnings, Eurozone shares benefited from their comparatively low valuations and the re-emergence of investors’ appetite for risk. However, no significant headway was made in terms of European and Swiss corporate profits. With a gain of 9.5 per cent, Switzerland’s benchmark SMI index was one of the world’s best performers in 2014.

The dollar-based MSCI Emerging Markets Index recorded significant drops both in September and in December. Its annual performance of –2.1 per cent was mainly attributable to a rebound in its underlying currency (USD); however, investors with the Swiss franc as their reference currency enjoyed a 9.3 per cent gain (including dividends) in this index.

Investors especially favoured large-cap companies with a clear focus on growth. At the sector-specific level, the standout performers were in the health care industry as well as the US IT sector. The clear losers were energy and raw materials stocks – both sectors suffered from the dramatic collapse in commodity prices.

The willingness to accept risk remained relatively high through- out the year. Short-term technical price declines were recouped within a matter of weeks. The S&P-based volatility index (VIX) actually fell to its lowest annual level since 2007.

The shares of VP Bank

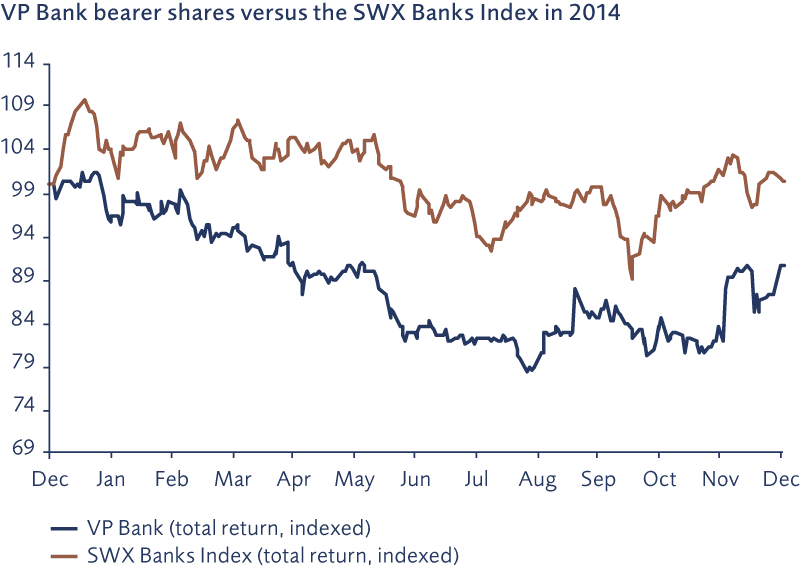

VP Bank shares have been listed on Switzerland’s stock exchange (SIX Swiss Exchange) since 1983. The company’s average market capitalisation in 2014 amounted to CHF 503 million, with the share price fluctuating between CHF 74.40 (August) and CHF 98.95 (January). The average price for the year (closing levels) was CHF 84.88. In 2014, VP Bank paid a dividend of CHF 3.50 per bearer share. The resulting dividend yield therefore exceeds that of both the overall Swiss market and the average for the banking industry in general.

VP Bank shares declined in value by roughly 9 per cent (including dividends) for the year, thereby underperforming the overall market as well as the banking index. The price losses were recorded mainly in the first half of the year. As of June, the share price traded in a sideways channel. In response to the announcement of VP Bank’s merger with Centrum Bank, the stock moved modestly higher in December.

Investor relations

The goal of VP Bank’s investor relations efforts is to foster an open, ongoing dialogue with shareholders and other capital market participants by providing them with a true and fair view of VP Bank Group, while also informing the interested public promptly about the latest developments at the company.

The tasks involved in this investor relations work include conducting discussions with analysts and investors, disclosing ad hoc information regarding business issues of relevance under securities law, producing the company’s annual and semi-annual reports and publishing the related financial results, as well as organising the annual general meeting of shareholders.

These investor relations activities were intensified further in 2014. Numerous analyst and media conferences were important events for fostering greater interaction and discussions with investors and financial intermediaries. In 2014, the first-ever VP Bank Investors’ Day was held in Liechtenstein, and further events of that nature are being planned.

Regular presentations addressing the current trend in financial results serve to enhance the dialogue with institutional and private investors. An additional means of communication is the website vpbank.wsc.ch, where all up-to-date information on VP Bank can be accessed.

The 2013 annual report of VP Bank was once again the recipient of a number of awards in 2014. In a comparison of annual reports from 226 companies in Switzerland and Liechtenstein, a jury comprised of communication and financial professionals ranked VP Bank Group’s report as one of the twelve best as a part of the “Swiss Annual Report Ratings 2014”. In connection with the “Galaxy Awards” of the “International Academy of Communications Arts and Sciences”, the 2013 annual report was named a “Gold Winner”. It also received a “Gold Award” within the scope of the international “Spotlight Awards” ceremony organised by the “League of American Communications Professionals”.

Further international acclaim for the annual report was evidenced by a “Silver Award” in the “Vision Awards” as well as by being named a “Bronze Winner” in the global “ARC Awards” annual report competition. The online version of VP Bank Group’s annual report was also a winner: it won silver in the “Vision Awards” and bronze in the “Best Annual Reports” category of the “Stevie Awards”. These accolades attest to the high quality of VP Bank Group’s information policy.

In 2014, Standard & Poor’s reconfirmed its “A–” (A–/A–2) rating of VP Bank Group. In terms of the outlook for VP Bank, the rating agency adjusted its view from “Stable” to “Negative” on 30 April 2014 and confirmed this opinion on 8 August 2014. In its report, however, Standard & Poor’s makes special note of VP Bank Group’s outstanding capitalisation, as well as its stable client base and shareholder structure.

This good “A–” rating confirms the solid and successful business model of VP Bank Group. VP Bank is one of the few private banks in Liechtenstein and Switzerland that are evaluated by a major international rating agency.

Research coverage of VP Bank Group is provided by analysts at MainFirst Bank AG and Zürcher Kantonalbank.

Agenda |

|

Publication of 2014 annual results | Tuesday, 3 March 2015 |

Extraordinary general meeting | Friday, 10 April 2015 |

Annual general meeting | Friday, 24 April 2015 |

Dividend payment | Thursday, 30 April 2015 |

VP Bank Investors’ Day | Wednesday, 20 May 2015 |

Publication of 2015 semi-annual results | Tuesday, 25 August 2015 |

Publication of 2015 annual results | Tuesday, 8 March 2016 |

|

|

VP Bank share details | |

Bearer shares, listed on SIX Swiss Exchange | |

Amount listing | 5,314,347 |

Free float | 53.12% |

Symbol on SIX | VPB |

Bloomberg ticker | VPB SW |

Reuters ticker | VPB.S |

Security number | 1073721 |

ISIN | LI0010737216 |

|

|

Share-related statistics 2014 |

|

High (23/01/2014) | 98.95 |

Low (25/08/2014) | 74.40 |

Year-end close | 85.00 |

Average price | 84.88 |

Market capitalisation in CHF million | 503 |

Consolidated net profit per bearer share | 3.45 |

Price/earnings ratio (PE) | 24.65 |

Dividend per bearer share (proposed) | 3.00 |

Net dividend yield in % | 3.5 |

Standard & Poor’s rating | A (A–/Negative/A–2) |

Contact

Tanja Muster · Head of Group Communications & Marketing

T +423 235 66 55 · F +423 235 65 00